Social Sharing block

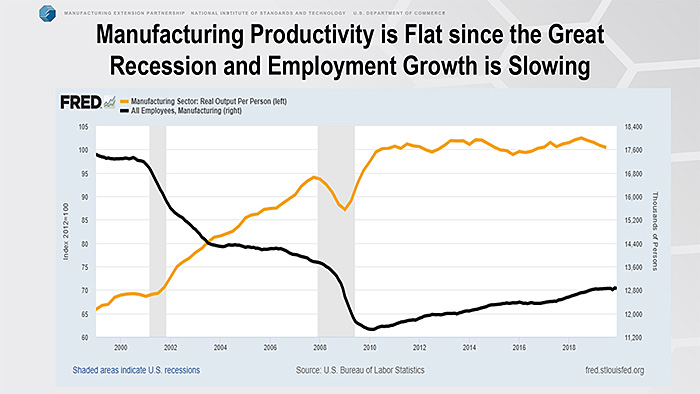

I find that every so often it is good to step back and think about the current state of manufacturing in the broadest sense. We all see bits and pieces as part of our daily work with manufacturers across the country and from reading the news, but sometimes it can be difficult to fit those puzzle pieces into the whole.

|

ADVERTISEMENT |

This is the day I break out my trusty old charts and graphs and data points to try and work some augury on where we may be headed.

Overall, most indicators show the manufacturing landscape slowing. Whether the slowdown is a temporary aberration (we saw similar patterns in 2016, for example) remains to be seen. The current data do, of course, reflect some large OEMs (GM and Boeing, in particular) slowing production, the trade dispute with China, and an economic slowdown globally, concurrent with the one we’re experiencing here.

…

Add new comment