| by Craig Cochran

Most sane people wouldn't consider steering a ship by looking backward, but that's exactly what most companies do when they focus entirely on financial measures for decision making. The balanced scorecard, one of the most significant management philosophies of the last quarter-century, confronts that stratagem head-on with a simple core concept: Stop trying to manage your organization by financial measures alone. Why? Because financial measures always look backward. They tell you what happened last month, last quarter or last year, but they say little about what will happen in the future.

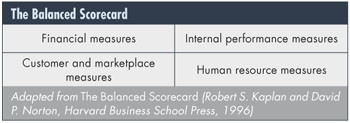

Financial measures are important, but so are others. Robert S. Kaplan and David P. Norton, authors of The Balanced Scorecard (Harvard Business School Press, 1996), advocate the use of a balanced portfolio of business measures. What exactly is a balanced scorecard? It's a model of metrics, with four boxes representing different measurement categories. The four categories drive performance across different time frames: short, medium and long term. The intent is that organizations will analyze their performance across all four categories of metrics instead of just analyzing and acting on financial measures. Focusing on a balanced portfolio of measures will drive improvement over the long term. Anyone with any amount of business experience knows that financial success in the short term doesn't always translate into long-term success, and that's the underlying wisdom of the balanced scorecard.

The specific measures that reside within each box of the balanced scorecard will be different from one organization to the next. In fact, one of the challenges of the balanced scorecard is in determining logical measures and getting accustomed to acting on them. Here's a summary of the four boxes and how they relate to one another:

• Financial measures. These metrics drive performance over the short term because actions taken to improve financial measures show results quickly. Examples include revenue, profit and cash flow. Financial measures are important because they represent the immediate survival of the organization. They are usually considered the starting point for any balanced scorecard.

• Internal performance measures. These drive achievement in the medium term because actions take longer to show results. Examples include efficiency, innovation and inventory turnover. Internal performance measures rarely show up on financial and accounting reports, but they indicate how well the organization manages its internal processes. Success on internal performance measures will have a direct, positive effect on financial measures, but the effect may take a number of months to appear.

• Customer and marketplace measures. These drive success over the medium to long term because actions might take months or years to show tangible results. Examples include customer perceptions, brand loyalty and market share. Customer and marketplace measures look at success through the eyes of customers, a point of view that is often ignored or minimized. These directly affect financial measures but shift gradually over time. Once customer perceptions begin to move, their momentum is hard to control. This underlies the importance of having a strong grip on what customers really think and what the organization plans to do about it.

• Human resource measures. These drive success over the long term because actions might take years to show tangible results. Examples include hours of training per employee, employee survey results and employee retention rates. Human resource measures are possibly the furthest removed from financial measures because they're often difficult to trace back to bottom-line numbers. But make no mistake---how well an organization manages its human resources certainly affects financial success.

Building a Balanced Scorecard: A Case Study

Chem-Pro, a manufacturer of polymer-based industrial products, had recently reorganized to become more customer-focused. Its traditional functional organization had been replaced by one designed around lines-of-business (LOB) and business processes. In addition, senior management had also identified four critical business processes that it must improve and excel at: order generation, product management, order fulfillment and production. Each of the five lines-of-business had different requirements for the four processes. For example, the consumer group distributed large numbers of standardized products through retail channels, while the precision group worked with the engineers of a small number of very large customers to define the product specifications for new chemicals. Obviously, each of the four critical business processes had to be customized to the different needs of each LOB.

The balanced scorecard for Chem-Pro began by defining a standard corporate template that clarified the strategic priorities for all the LOBs in the new organization. Each line-of-business then developed its particular strategy, consistent with corporate priorities. At that stage, the LOB scorecards were communicated to the new managers of the four business processes so that they could develop programs that would meet the specific objectives of the individual LOBs. The sequential process of defining objectives and measures at t he corporate level, linking corporate objectives to individual LOB objectives and measures, and linking LOB objectives and measures to critical business processes enabled Chem-Pro to introduce a complex organizational change--from functional specialization to customer- based line-of-businesses and customer-focused business processes--in a manner that gained acceptance, buy-in and involvement by everyone.

--from The Balanced Scorecard (Robert S. Kaplan and David P. Norton, Harvard Business School Press, 1996) |

Organizations should try to produce effective results not just for next month but also next year and next decade. Actions taken to improve medium- to long-term metrics are investments in the organization's future. Other themes of the balanced scorecard include linking metrics to strategy, communicating metrics to all personnel and regular progress reviews. These common-sense concepts fit perfectly with the ISO 9001 requirement for measurable objectives.

Are you ready to build a balanced scorecard for your organization? If so, here are some steps that will help ensure success.

The balanced scorecard represents a significant shift in the way organizations gauge their performance. For this reason, top management must embrace the concept fervently enough to become its primary champion. This kind of sales job is no small feat. How do you generate such enthusiasm for a seemingly radical concept? Here's one path:

• Describe what the organization is doing now, which is using financial measures primarily to make all decisions. Show how this has led to shortsighted decisions and mistakes. Make sure to be very diplomatic in how these problems are portrayed.

• Describe the balanced scorecard and explain why it's superior to the measurement methods used by most organizations. Discuss companies that have utilized the concept and provide examples of the measures they used. Make sure to mention that the measures on a balanced scorecard are derived directly from the organization's strategy, which links them perfectly with long-term success.

• Describe how the balanced scorecard could be used in your organization. Outline the strategic benefits to managing a balanced portfolio of measures that drive performance over the short, medium and long term. Explain how a balanced scorecard would remove the ambiguity and confusion that usually accompany the deployment of strategy.

Get top management energized by the concept. Having top management's ear can be very helpful. To achieve this, your sales job is actually twofold: You must sell the people who have top management's ear and then have them assist you in selling top management. The concept almost sells itself when presented correctly. Kaplan and Norton's book can facilitate your preparation, as can a number of others. If you've sold yourself on the concept and truly believe in it, then you'll be in a good position to spread that enthusiasm.

Your best allies during this sales and education process can be your finance people. This might sound a little strange because these would seem to be the people with the most to lose from focusing on things other than financial measures. A smart CFO understands the pitfalls of managing for the short term, though. Use the financial leaders in your organization as sounding boards. It's likely that they'll see the obvious benefits of the approach. Once you have the finance people convinced, your president or CEO should be easy.

After top management has become engaged by the concept, someone has to do the dirty work--i.e., build the scorecard itself. A project of this sort will be challenging because the metrics of the past and present might not be much help. The starting point is the organization's strategy. What broad actions are you taking during the next year to stay competitive? The measures on the balanced scorecard will support the strategy, examining it from the perspectives of four quadrants: financial, internal performance, customers and the marketplace, and human resources. That means you'll have to go to the process owners and stakeholders who are tied to these perspectives. Typically, these are the people who are best prepared to assist in developing the respective parts of the balanced scorecard:

• Financial measures: finance, accounting, top management and sales

• Internal performance measures: production, design, quality assurance, engineering, purchasing and logistics

• Customer and marketplace measures: sales, marketing and customer service

• Human resource measures: human resources, training, health and safety

Note that top management is present in only one of these groups. This is so it won't unduly influence measures in the other three groups. There's no benefit to upholding the paradigms of the past when building a scorecard.

The best way to engage each group is through a facilitated session during which you guide participants through an exploration of their own experiences and knowledge about the issues at stake. If the organization has a well-defined strategy, this process is relatively simple. What measures will support achieving the strategy? Define these from each of the four quadrants, and the resulting set of measures will become your balanced scorecard.

The problem is that many organizations don't have a well-defined strategy. Some never get around to doing strategic planning at all. In that kind of organization, developing a balanced scorecard will prove challenging. Even when there's an existing strategy, it's often the result of "group think" or has little connection to the organization's practical requirements.

I recommend holding a series of facilitated meetings with representatives from the four groups listed earlier. During these sessions, you'll guide the participants through a SWOT (strengths, weaknesses, opportunities and threats) analysis specifically focused on their functional areas. For example, participants in the customer and marketplace group will examine strengths, weaknesses, opportunities and threats through the eyes of their customers. The resulting measures will seek to maximize strengths and opportunities, and minimize weaknesses and threats, as viewed through their customers' perceptions. Here are some of the questions in each of the balanced scorecard sections:

• Customer and marketplace SWOT analysis:

--In the eyes of our customers, what do we do especially well?

--What was our biggest customer service success last year?

--What problems do customers keep telling us about?

• Human resource SWOT analysis:

--What makes our people better than employees in other organizations?

--What employee skills and abilities could be improved?

--What skills and abilities do we think will be critical 10 years from now?

• Internal process SWOT analysis:

--What part of our organization experiences the least waste? What enables this efficiency?

--What efficiencies do our competitors have that we don't? What could we do to adopt these efficiencies?

--What's one process improvement we could implement that would put us ahead of the competition?

• Financial SWOT analysis:

--What financial assets do we manage especially well?

--What problems do our accountants keep telling us about?

--What financial advantages do our top competitors have we that we don't?

--What are the three most likely ways our capital could dry up in the next

five years?

The full versions of these SWOT worksheets are available for download:

Each of the SWOT analyses will produce a set of measures. Not all the measures will appear on the final scorecard, of course, but at least one measure from each group will. The groups can trim their lists through a multivoting methodology (i.e., where each group member casts a predetermined number of votes) or through a more quantitative process. A tool called the proposed measures evaluation worksheet is also available at Quality Digest's Web site. Regardless of the method used to select your final measures, keep your list short. Having a punchy list of five to 10 measures will clearly communicate to everyone what matters most. If you adopt more than 10 measures for your balanced scorecard, the focus becomes diminished. People are able to concentrate on only a few things at a time, so don't overcomplicate the process. If your balanced scorecard is linked to your competitive reality, then it can be an indispensable tool to drive your long-term success.

Craig Cochran is a project manager with Georgia Tech's Economic Development Institute. He's an RABQSA-certified QMS lead auditor and the author of Customer Satisfaction: Tools, Techniques and Formulas for Success and The Continual Improvement Process: From Strategy to the Bottom Line, both available from Paton Press (www.patonpress.com). QD

|